》View SMM Copper Prices, Data, and Market Analysis

》Subscribe to Access SMM Historical Spot Metal Prices

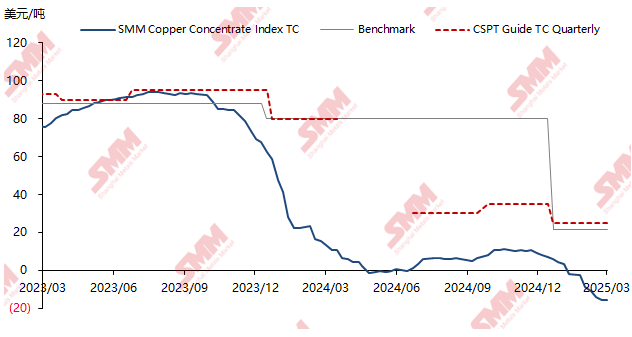

It is well known that since the end of 2023, the global copper concentrate market has experienced a severe supply-demand imbalance. The tight spot supply of copper concentrates in the Chinese market has become increasingly acute, as evidenced by the sharp drop in the SMM Copper Concentrate Spot Index. On March 14, the SMM Imported Copper Concentrate Index (weekly) was reported at -$15.92/mt, down $0.09/mt from the previous week's -$15.83/mt.

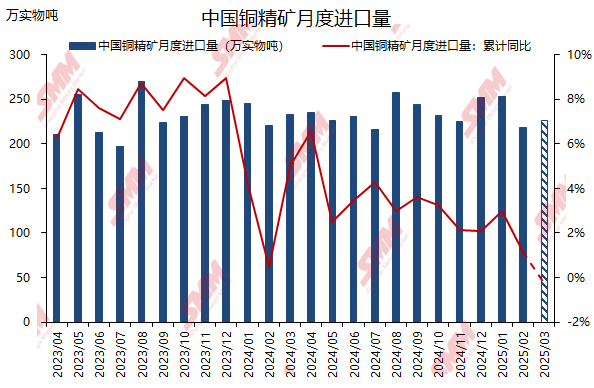

On March 18, 2025, the General Administration of Customs of China released the monthly import data for copper concentrates for January and February 2025: In January 2025, China imported 2.58 million mt of copper ores and concentrates, up 0.32% MoM and up 2.98% YoY; in February 2025, China imported 2.18 million mt of copper ores and concentrates, down 13.83% MoM, with a cumulative YoY increase of 1.13%. If Indonesia's copper concentrate exports proceed smoothly, SMM expects China's copper concentrate imports in March 2025 to reach 2.25-2.3 million mt.

According to SMM, the Indonesian government announced on Monday that it had issued a six-month copper concentrate export license to Freeport Indonesia. Today, Freeport Indonesia stated that it had obtained an export license for 1.27 million mt of copper concentrates from the Indonesian Ministry of Trade, allowing shipments from Papua Port to commence. Meanwhile, on March 13, the President of Panama announced the approval of the export of 120,000 mt of Cobre Panama copper concentrates.

While these seemingly favorable policies may alleviate the tight spot supply in China's copper concentrate market, today's market rumors about BHP's Escondida tender results—at -$25.5/dmt for smelters and -$53/dmt for traders—have further exacerbated the already deteriorating spot market. However, SMM believes that these "double blessings" may have a stabilizing effect in the short term but are ultimately insufficient to reverse the rapidly worsening spot market in the long term. On one hand, China's annual imports of copper concentrates from Indonesia have historically accounted for only 1%-3%, with 2024 imports totaling 550,000 mt, representing just 1.95%. Moreover, Grasberg's primary customer countries are Japan, South Korea, and European nations. Although Indonesia's copper concentrate inventory has reached an astonishing 1.3 million mt, most of this volume is unrelated to China. On the other hand, Panama's 120,000 mt of Cobre Panama copper concentrates are already "spoken for," with the 120,000 mt destined for South Korea's Onsan smelter and three Japanese smelters, leaving none for the Chinese market.

》Click to View the SMM Copper Industry Chain Database